When you take out a mortgage to purchase a home, you’re likely to interact with both a mortgage lender and a mortgage servicer during the life of your loan. While both are essential players in the mortgage process, many homebuyers confuse the two or fail to understand the distinct roles they each play. Understanding the differences between mortgage lenders and mortgage servicers is crucial for navigating your mortgage journey, from applying for the loan to managing payments. This article will explain what mortgage lenders and mortgage servicers do, how they differ, and how they impact your mortgage experience.

What is a Mortgage Lender?

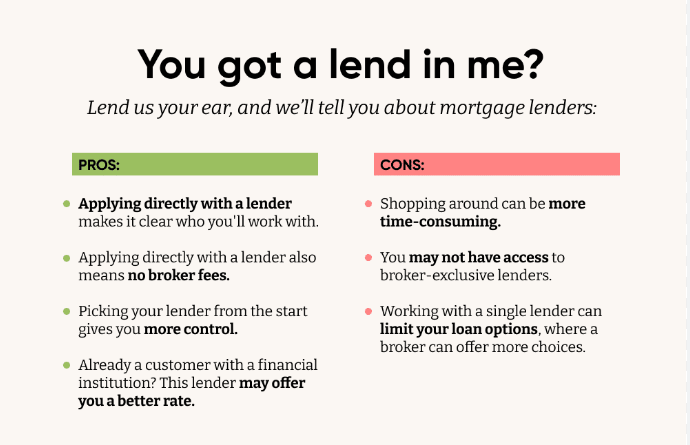

A mortgage lender is a financial institution or individual that provides the funds necessary to purchase a home. They are the initial source of the money you borrow and typically include banks, credit unions, mortgage banks, or other financial organizations. Mortgage lenders are responsible for evaluating your financial situation, approving or denying your mortgage application, and offering you the terms of your loan.

The Role of a Mortgage Lender:

- Loan Origination: The first and most important role of a mortgage lender is to originate the loan. This involves reviewing your application, verifying your financial details, and assessing your ability to repay the loan. Lenders evaluate factors such as your credit score, income, debt-to-income ratio, and employment history to determine whether you qualify for a mortgage and what type of loan is suitable for your needs.

- Loan Approval: Once you apply for a mortgage, the lender will review your application and documentation (such as tax returns, bank statements, and employment verification) to assess your financial stability. If everything checks out, they will approve the loan and issue you a commitment letter outlining the terms of your mortgage, including the interest rate, loan amount, and repayment period.

- Setting Terms and Interest Rates: Mortgage lenders decide the terms of your loan, including whether it will be a fixed-rate or adjustable-rate mortgage, the duration of the loan (e.g., 15 years, 30 years), and the interest rate. These terms can significantly affect your monthly payment and the total amount you’ll pay over the life of the loan.

- Disbursing Funds: After you’ve accepted the loan offer and completed the closing process, the mortgage lender provides the funds for the home purchase. These funds are typically paid directly to the seller, and the lender then holds a lien on the property until the loan is repaid.

Mortgage Lender’s Responsibilities:

- Approval and underwriting of your loan application

- Funding the loan for the home purchase

- Setting loan terms (interest rate, repayment period, etc.)

- Handling the closing process and distributing funds

What is a Mortgage Servicer?

A mortgage servicer is a company or entity responsible for managing your mortgage after it has been originated. In most cases, the mortgage servicer is a third-party company that works on behalf of the lender or the investor who owns the loan. The servicer handles the day-to-day management of your mortgage, including processing payments, managing escrow accounts, and handling any issues that arise during the life of the loan.

The Role of a Mortgage Servicer:

- Managing Monthly Payments: Once your loan is in place, the mortgage servicer collects your monthly mortgage payments. These payments usually cover both the principal balance of the loan as well as interest, property taxes, homeowners insurance, and possibly private mortgage insurance (PMI). The servicer is responsible for distributing these payments to the appropriate accounts. For example, they ensure the correct portion of your payment goes toward reducing the loan balance, while other portions go into your escrow account to cover taxes and insurance.

- Escrow Management: Many mortgage loans include an escrow account, which is used to collect and disburse funds for property taxes and insurance premiums. The mortgage servicer manages this account, collecting monthly payments from you and paying your taxes and insurance bills when they are due. If there’s a shortfall in the escrow account, the servicer may adjust your monthly payments accordingly.

- Customer Service: Mortgage servicers act as your point of contact throughout the life of the loan. If you have questions or need assistance, such as if you’re facing financial hardship or need to refinance, the servicer is the company you’ll interact with. They also help with setting up automatic payments, providing account information, and offering support if you encounter any issues with your mortgage.

- Handling Delinquencies: If you miss a payment or fall behind on your mortgage, the servicer will generally reach out to discuss options for getting your payments back on track. They may offer solutions such as loan modifications, forbearance, or repayment plans. In extreme cases, if you consistently miss payments, the servicer may begin foreclosure proceedings on behalf of the lender or investor.

- Mortgage Transfers: In many cases, the servicer you work with may not be the same company that originally funded your loan. Mortgage loans are frequently bought and sold between investors, and as a result, your loan may be transferred to a different servicer. While this can be confusing, the terms of your loan (such as the interest rate) will remain unchanged, and the new servicer will continue managing the day-to-day tasks of your mortgage.

Mortgage Servicer’s Responsibilities:

- Collecting monthly mortgage payments and distributing them

- Managing escrow accounts for property taxes and insurance

- Providing customer service and addressing inquiries about your loan

- Offering options if you face payment difficulties or foreclosure

- Managing loan transfers if the loan is sold to another servicer

Key Differences Between Mortgage Lenders and Mortgage Servicers

While the terms “lender” and “servicer” might seem interchangeable, they have distinct roles in the life cycle of a mortgage. Here’s a breakdown of the key differences:

| Mortgage Lender | Mortgage Servicer |

|---|---|

| Provides the funds for your loan | Manages the day-to-day management of the loan |

| Sets the loan terms (interest rate, repayment period) | Collects payments and distributes them to the correct accounts |

| Issues the loan and holds the lien on the property | Ensures property taxes and insurance premiums are paid on time |

| Typically involved in the closing process and funding | Handles customer service and provides assistance with payment issues |

| May sell or transfer the loan to another investor or servicer | May transfer your loan to another servicer, but does not alter the terms of the loan |

When to Contact Your Mortgage Lender vs. Your Mortgage Servicer

Knowing when to contact your lender and when to contact your servicer is crucial for ensuring your mortgage experience runs smoothly.

- Contact Your Mortgage Lender If:

- You need to apply for a new mortgage or refinance your existing mortgage

- You want to change the terms of your mortgage or negotiate your interest rate

- You have questions regarding your original loan agreement

- Contact Your Mortgage Servicer If:

- You need assistance with your monthly mortgage payments or want to set up automatic payments

- You have questions about your escrow account, property taxes, or insurance

- You’re facing financial difficulty and need to discuss loan modification or forbearance options

- You need customer service for general inquiries related to your loan

Conclusion

While mortgage lenders and mortgage servicers both play important roles in the mortgage process, they are responsible for different aspects of your loan. The lender provides the initial funds and terms for your mortgage, while the servicer handles the ongoing management of your mortgage payments, taxes, insurance, and customer service needs. Understanding these distinctions will help you navigate your mortgage journey more effectively and ensure you know who to contact for various issues. Whether you’re applying for a loan, making payments, or seeking assistance, recognizing the right point of contact can make all the difference.